This note is designed by the ‘Basics in Maths’ team. These notes to do help the TS intermediate first year Accountancy students fall in love with Accountancy and overcome the fear.

These notes cover all the topics covered in the TS I.P.E First year Accounyancy syllabus and include plenty of formulae and concept to help you solve all the types of Inter Accountancy problems asked in the I.P.E and entrance examinations.

Accounting is one of the fastest-growing not only in our country but also in the entire world. The accounting system provides relevant and reliable financial information parties.

1.BOOKKEEPING AND ACCOUNTING

INTRODUCTION

ACCOUNTING MEANING: Accounting is often called the “languages of business”. Accounting helps in communicating the financial information to various parties interested in it.

BOOK KEEPING: Bookkeeping is the branch of knowledge that concerned with the recording of business transactions. The basic objective of book keeping is to have a permanent record of all the business transactions. in specific terms, book keeping is defined as

“book -keeping is the science and of correctly recording in the books of account, all those business transactions that result in the transfer of money’s worth”.

OBJECTIVES OF ACCOUNTING:

The main objectives of accounting are:

• To maintain accounting records.

• To calculate the result of the operation.

• To ascertain the financial position.

• To communicate the information to users

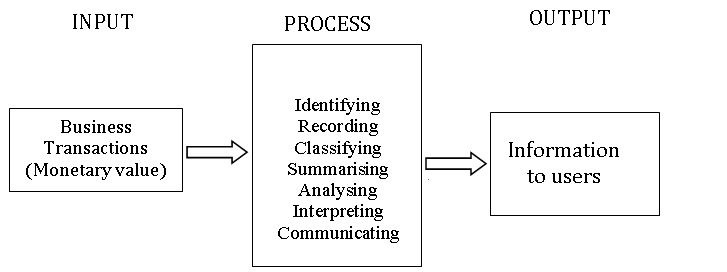

ACCOUNTING PROCESS

• The process of accounting is stated in the definition is explained as below:

1. Identifying: Identifying the business transactions from the source document.

2.Recording: The next function of accounting is to keep a systematic record of all business transactions, which are identified in an orderly manner, soon after their occurrence in the journal or subsidiary books.

3. Classifying: This is concerned with the classification of the recorded business transactions so as to transactions of similar type at one place, i.e., in a ledger(a book of accounts) by extracting the balance/total of accounts.

4. Summarizing: It is the process of finding the totals of balances of all accounts so as to prepare a trial balance.

5. Reporting: the classified information available from the trial balance is used to prepare a profit and loss account and balance sheet in a manner useful to the users of accounting information.

6. Analyzing: It establishes the relationship between the items of the profit and loss account and the balance sheet. the purpose of analyzing is to identify the financial strength and weakness of the business. it provides the basis for interpretation.

7. Interpreting: It is concerned with explaining the meaning and significance of the relationship so established by the analysis. interpretation should be useful to the users, so as to enable them to take the correct decisions.

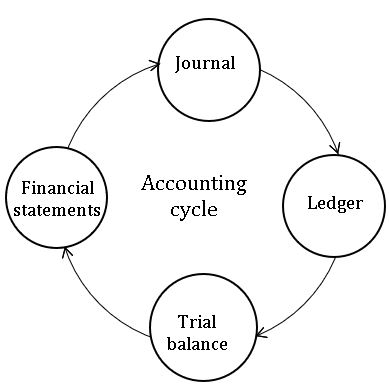

ACCOUNTING CYCLE

An accounting cycle is a complete sequence of accounting process that begins with the recording of business transactions and ends with the preparation of final accounts.

These include Journal, Ledger, Trial Balance and financial statements such as Trading account, profit and loss account balance sheet.

The accounting cycle is depicted in the following diagram:

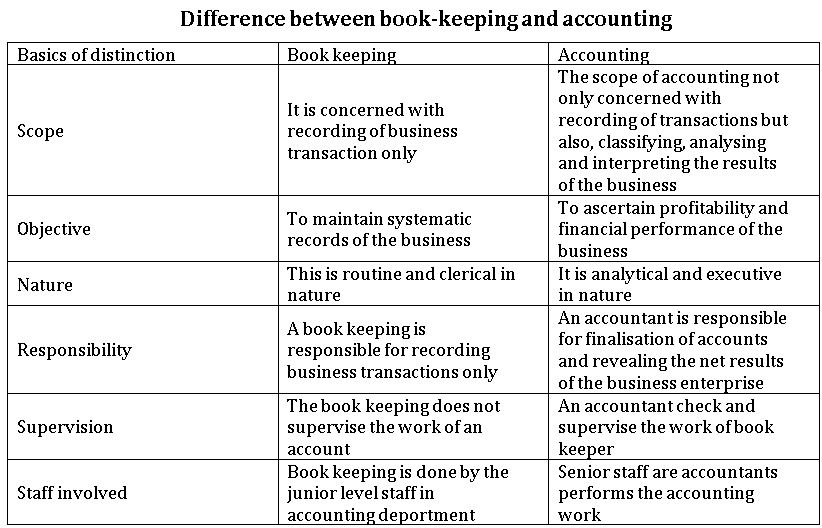

Accountancy, Accounting and bookkeeping:

Accountancy:- refers to a systematic knowledge of accounting which covers rules, regulations, principles, concepts and conventions, and standards that govern the accounting process.

Accounting: – refers to the actual process of preparing and presenting the accounting information. In other words, it is an art of putting the academic knowledge of accountancy into practice.

Book- keeping: – is a part of accounting and is concerned with record keeping or maintenance of books of accounts. Is often routine and clerical in nature.

ADVANTAGES ACCOUNTING:

1.Permanent and reliable record: Accounting provides a permanent record for all business transactions and provides reliable information to different interested parties thus, replacing the money which fails to remember everything.

2.Net results of business operations: Accounting provides the final result (profit or loss) of business for a given period of time.

3.Ascertainment of financial position: It is not enough to know only the profit or loss, but the proprietor requires a full picture of his financial position to plan for next year ‘s business.

4.Facility of comparative study: Accounting provides the facility of the comparative study of the various aspects of business such as profit, sales, expenses, etc with that of the previous year and helps the businessman to take necessary decisions.

5.Control over assets: In the course of business, the proprietor acquires various assets like building, machinery, furniture, etc. which are well protected generating records.

LIMITATIONS OF ACCOUNTING:

1.Records only monetary transactions: Accounting considers monetary transactions only, non monetary transactions like, quality, organization culture, units of production sales, etc are ignored in accounting.

- Historical in nature: Accounting considers only historical transactions i.e. transactions that have occurred in the past only recorded in accounting books. Transactions relating to future estimation and forecasts are not considered in accounting.

- Price level changes are not considered: Accounting does not consider price level changes which may occur from time to time, thus, it doesn’t reflects the current position.

4.Does not provide realistic information: While preparing the books of account, the subjectivity of the accountant may influence the final results of the business enterprise. This may not provide realistic information which in turn affects the overall results of the business concern.

BASIC ACCOUNTING TERMS

- Account

- Accounting entry

- Transactions

- Accounting period

- Proprietor

- Capital

- Assets

- Liabilities

- Drawings

- debtors

- creditors

- purchase

- sales

- stock

- revenue

- expenses

- Income

- Voucher

- receipt

2.ACCOUNTING PRINCIPLES

Accounting principles: The accounting principle are the general accounting procedure practices which guide the accountancy in the preparation of accounting records. Accounting principles can be broadly classified into accounting concepts and accounting conventions.

Accounting concepts are as follows:

- Business entity concept: As per this concept, business organizations are treated as a separate entity which can be distinguished from the “owners” or stakeholders who provide capital to it. This concept helps in keeping the private affairs of the owns and stakeholders separate from the business affair.

- Dual aspect concept: Dual aspect principle is the basics for a double-entry system of book-keeping. All business transactions recorded in accounts have two aspects: receiving a benefit and giving benefits. For example, when a business acquires an asset (receiving of benefit) it must pay cash (giving of benefit).

- Going concern concept: As per this concept it is assumed that the organizations will continue for a long time, unless and until it has entered into a state of liquidation. The financial statements are prepared at defined period end to measure the performance of the entity during that period and not on the closure or liquidation of the entity.

- Money measurement concept: In accounting, all the transactions are recorded in terms of money in other words, events or transactions that cannot be expressed in terms of money are not recorded in the books of accounts. Receipts of income, payments of expenses, purchase and sale of assets etc., are monetary transactions that are recorded in the books of accounts. whereas, the events of machinery breakdown is not recorded as it does not have a monetary value. However, the expenditure incurred for the repair of the machinery can be measured in monetary value and hence is recorded.

- Cost concept: as per this concept, an asset is ordinarily recorded at the period to acquire it, i.e., at its cost and this cost is the basis for all subsequent accounting for the assets. The assets recorded at cost at the time of purchases may systematically be educed through depreciation.

- Accounting period concept: An accounting period is the interval of time, at the end of which the financial statements are prepared to ascertain the financial performance of the organization. The preparation of financial statements at periodic intervals help in taking timely corrective action and developing appropriate strategies. The accounting period is normally considered to of twelve months and the accounting books are closed at the end of every year either at the end of march or December.

- Accrual concept: Under the cash system of accounting, the revenues and expenses are recorded only if they are actually received or paid in cash, irrespective of the accounting period to which they belong. But under the accrual concept, occurrence of claims and obligations in respect of incomes expenditures, assets or liabilities based on happening of any event, passage of time, rendering of services, are recorded even though actual receipts or payments of money may not have taken place. In respect of an accounting period, the outstanding expenses and the repaid expenses and similarly the income receivable and the income received in advance are shown separately in the books of accounts under the accrual method.

- Matching concept: matching the revenues earned during an accounting period with the cost associated with the period to ascertain the of the business concern is called the matching concept. It is the basis for finding accurate profit for a period which can be safely distributed to the owners.

- Realisation concept: Accounting to this concept, revenue should be accounted for only when it is actually realized or has become certain that the revenue will be realized. This signifies that revenue should be recognized only when services are rendered or the sale is affected. However, in order to recognize revenue, actual receipt of cash is not necessary, but the organization should be legally entitled to receive the amount for the services rendered or the sale affected.

ACCOUNTING CONVENTIONS

Accounting conventions are the customs or traditions guiding the preparation of accounts. They are adopted to make financial statements clear and meaningful. Following are the four-accounting convention:

- Convention of disclosure: accounting statements should disclose fully and completely all the significant information, based on which, decisions can be taken by various interested parties, it involves proper classification and explanations of accounting information which are published in the financial statements.

- Convention of materiality: The materiality principle requires the disclosure of the significant information, exclusion of which would influence the decisions. Unimportant and insignificant information are either left out or merged with other items.

- Convention of consistency: The convention of consistency facilitates comparison of financial performance of an entity from one accounting period to another which is financial performance of an entity from one accounting period to another, which is possible when the accounting principles following by an entity are consistently applied over the years. For example, an organization should not change its method of depreciation every year, i.e., from straight line method to written down value method or vice versa. Similarly, the method adopted for valuation of stock, viz., First in First out (FIFO)or last in First out (LIFO)should be consistently followed.

- Convention of conservatism: As per this convention, he anticipated profits should be ignored but all the anticipated losses should be considered into the books of accounts of an entity. The essence of his principle is “anticipate no profit and provide for all possible losses”. This means that all prospective losses are taken into consideration, however, no doubtful income is taken into consideration in the recording of transactions by an entity.

3.Double Entry Book Keeping System

Introduction

Lucas Pacioli, an Italian merchant, first articulated the double-entry system in 1994 A.D. Though the system of recording business transactions in a systematic manner has originated in Italy, it was perfected in England and other European countries during the 18th century only i.e., after the industrial revolution. Many countries have adopted this system today for recording the transactions.

MEANING

There are numerous transactions which are to recorded in a business concern. Each transaction, reveals two important aspect: one aspect is “receiving aspect” or “incoming aspect” or” expenses/loss aspects”, termed as the “debit aspect”. The other aspect is “giving aspect” or “outgoing aspect” or “incoming/gain aspect”, termed as the “credit aspect”, these two aspects, namely” debit aspect” and “credit aspect”, forms the basics of double entry system. Hence, the double entry system involves the recording of both of the aspects of a transaction ie., debit and credit.

The fundamental rule under double entry book keeping system is that. ‘for every debit there must be corresponding value of credit’.

According to J.R. Batliboi “every business transaction has a two-fold effect and that it affects two accounts in opposite directions and if a complete record were to be made of each such transactions, it would be necessary to debit one account and credit another account. This recording of the twofold effect of every transaction has given rise to the term double entry system”.

FEATURES

- Every business transaction affects two accounts

- Each transaction has two aspects, i.e., debit and credit

- It is based upon accounting assumptions, concepts and principles

- It helps in preparing trial balance which is a test of arithmetical accuracy in accounting.

- Finally it helps in preparation of final accounts with the help of trial balance

ADVANTAGES

1.COMPLETE RECORD OF TRANSACTION: – This system maintains a complete record of all business transactions, because it records both the aspects of financial transaction.

2.SCIENTIFIC SYSTEM: -This is the only scientific system of recording business transactions. It helps to attain the objectives of accounting.

3.ACHECK ON THE ACCURACY OF ACCOUNTS: – By the use of this system, the accuracy of the accounting work can be established by the preparation of trial balance.

- Prevents frauds and errors: – In case of disagreement of trial balance, efforts will be made to locate the errors by internal check, so that correct picture of the business may be ascertained.

- Ascertainment of profit or loss: – It helps in ascertainment of profit or loss for a particular period by preparing the profit and loss account.

- Ascertainment of the financial position: – The financial positions of the concern can be ascertained at the end of each period by preparing balance sheet.

- Full details for control: – This system permits accounts to be kept in a very detailed from, and thereby provides sufficient information for the purpose of control.

- Comparative study: – The results of one year may be compared with those of previous years and the reasons for change may be ascertained.

- Helps in decision making: – This system provides sufficient information to the management for making decisions.

ACCOUNT

Every transaction has two aspects and each aspect has an account. It is stands that’ an account is ‘a summary of relevant transaction at one place relating to a particular head’.

The common form of an account has three parts;

- A ’Title’ that describes the name of the asset, liability, or equity account.

- A ’Left side’ or the ‘debit side’.

- A ’Right side’ or the ‘credit side’.

This form of account is called is a ‘T’ account because of its similarity to the letter ‘T’ as shown below

DEBIT AND CREDIT

Accountant uses the terms ’debit and credit’, to refer to left side and right side of an account respectively. to debit an account is to enter an amount on the left side of an account, and to credit an account is to enter an account on the right side of an account.

ACCOUNTING EQUATION

Accounting equitation is based on dual aspects concept (Debit and Credit). The accounting equation shows the relationship between the economic resources of a business and the claims against those resources. At any given time, the following relationship holds:

Economic Resources= Claims

The simplified accounting equation is shown below.

ASSETS= EQUITIES

(OR)

ASSETS= CAPITAL+LIABILITIES (A=C+L)

CAPITAL=ASSETS-LIABILITIES (C=A-L)

LIABILITIES = ASSETS- CAPITAL (L= A-C)

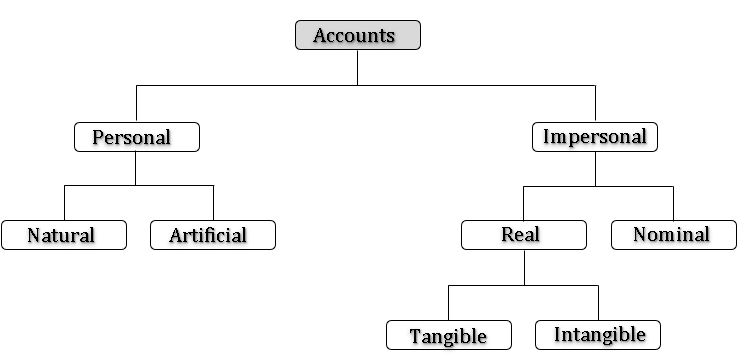

Classification of accounts:

- Transactions relating to individuals and firms

- Transactions relating to properties, goods or cash.

- Transactions relating to expenses or losses and incomes or gains.

Therefore, accounts can also be classified into personal, real and nominal. The classification may be illustrated as follows:

PERSONAL ACCOUNTS: – The accounts which related to individuals or personal are known as personal accounts. Personal accounts include the following;

1.Natural person: – accounts which relate to individuals.

For example: – Abhi a/c, Anu a/c etc.

2.Artificial persons: – accounts which related to a group of persons or firm or institutions.

For example: – Infosys td., Andhra Bank, life insurance corporation of India, Lions club etc

NOTE: -the proprietor being an individual his capital account and his drawings accounts are also personal account.

IMPERSONAL ACCOUNTS: – All those accounts which are not personal accounts are impersonal accounts. This is further divided into two types viz. real and nominal accounts.

1 Real Accounts: – accounts relating to properties and assets which are owned by the business concern are, real accounts, which includes tangible and intangible accounts.

For example: – land, building, machinery, furniture, stock, goodwill etc.

2 Nominal Accounts: – Those accounts do not have any existence, form or share. They relate to incomes and expenses or gains and losses of a business concern. Salary accounts, commission accounts, rent accounts, discount accounts etc. are examples of nominal account.

Rules for DEBIT and CREDIT:

1 Personal accounts: -a) Debit the receiver

b) Credit the giver

2 Real accounts: – a) Debit what comes in

b) credit what goes out

3Nominal accounts: – a) Debit all expenses and losses

b) Credit all incomes and gains

4.JOURNAL

MEANING

A journal is a book in which an accounting transaction is written in accounting terms. Journal is called as ‘book of original entry’ or book of primary entry’ as all the transactions pertaining to a business are first entered in this book. In journal, transactions are entered in the chronological order i.e. in the sequence in which they occur

The process of recording the transaction in the journal is called “journalizing” and the entry made in the journal is called as “journal entry”.

PROFORMA

Date | particulars | L.F | Debit Amount Rs. | Credit Amount Rs. |

|

|

|

|

|

Date column: – the date on which the transaction is taking place is written in this column. The year and month is written only once in the beginning.

Particulars column: in this column, the name of the account to be debited is written in the first line and the name of the account to be credited is written in the second line prefixed with ‘To’ and explanation of the transaction for which the entry is recorded is written briefly in brackets, known as ’narration’.

L.F (ledger folio): – Ledge Folio means, page of the ledger in which the entry is posted.

Debit amount column: – In this column, the amount to be debited is written against the debit entry.

Credit amount column: – In this column, the amount to be credited is written against the credit entry.

NOTE: According to the principle of double entry system both debit and credit aspects of the transactions are recorded in the journal.

Conventionally, a journal is prepared in a specific format as shown below:

JOURNAL

Date | V/R | Particulars | L/F NO | Debit Amount (in Rs) | Credit Amount (in Rs) |

June 15th | – | Cash a/c Dr To capital a/c (being the amount brought in cash towards capital vide receipts No.-date) | – | 1,00,000 |

1,00,000 |

June 15th | – | Furniture a/c Dr To cash a/c (being the amount paid towards furniture purchased from M/s-) |

| 12,000 |

12,000 |

A journal Entry

June15th

| Furniture a/c Dr To cash a/c | 12,000 12,000

|

Visit my YouTube Channel: Click on Below Logo